Are you scouting for sector-based investment? Healthcare is one industry with significant returns in the last five years. The BSE Healthcare index, which comprises pharmaceuticals, biotechnology, healthcare, and medical devices major constituents such as Sun Pharmaceutical, Dr Reddy’s Laboratories, Cipla, and Divi’s Laboratories, has surged over 60 per cent in the last five years, and 16 per cent in over a year. The healthcare index rose by 27 per cent to its highest level (45806.79) in the last five years from the lower levels in the last year.

Analysts from a domestic brokerage have handpicked a scrip from the basket with nearly 15 per cent upside.

Analysts recommend buying Max Healthcare shares for one year

SBI Securities’ analysts have a ‘buy’ stance on Max Healthcare shares due to several reasons like capacity enhancement plans, diverse healthcare products, penetration in metro geographies, financial performance, and valuation.

Here are highlights of what the brokerage said:

- The company plans to add 1,464 beds, 299 beds and 2,122 beds in FY26, FY27 and FY28 respectively.

- It also plans to diversify its presence in Mumbai through an asset-light built-to-suit 500 bed hospital in Thane and expects to commission the hospital in CY28.

- Max Healthcare’s operations include high-margin specialty offerings including oncology, cardiac-sciences, orthopaedics, etc.

- As of 3QFY25, the company has the highest proportion of operating beds in key market of Delhi and Mumbai compared to its peers.

- Delhi and Mumbai have the high per capita income, insurance penetration, health awareness and propensity to pay for high end quaternary care facilities, resulting in higher Average Revenue per Operating Bed (ARPOB) compared to rest of the country.

Max Healthcare Share Price Target

The brokerage has recommended buying the Max Healthcare stock with a twelve-month target of Rs 1,256, implying a potential upside of 14.20 per cent in the period.

Does it have good valuations?

According to the brokerage, at the closing market price of Rs 1,092, the stock is trading at an FY26E/FY27E EV/EBITDA multiple of 47.0x and 36.6x, respectively.

The company is expected to maintain its growth trajectory, driven by increasing occupancy and the commercialisation of new beds, the brokerage added.

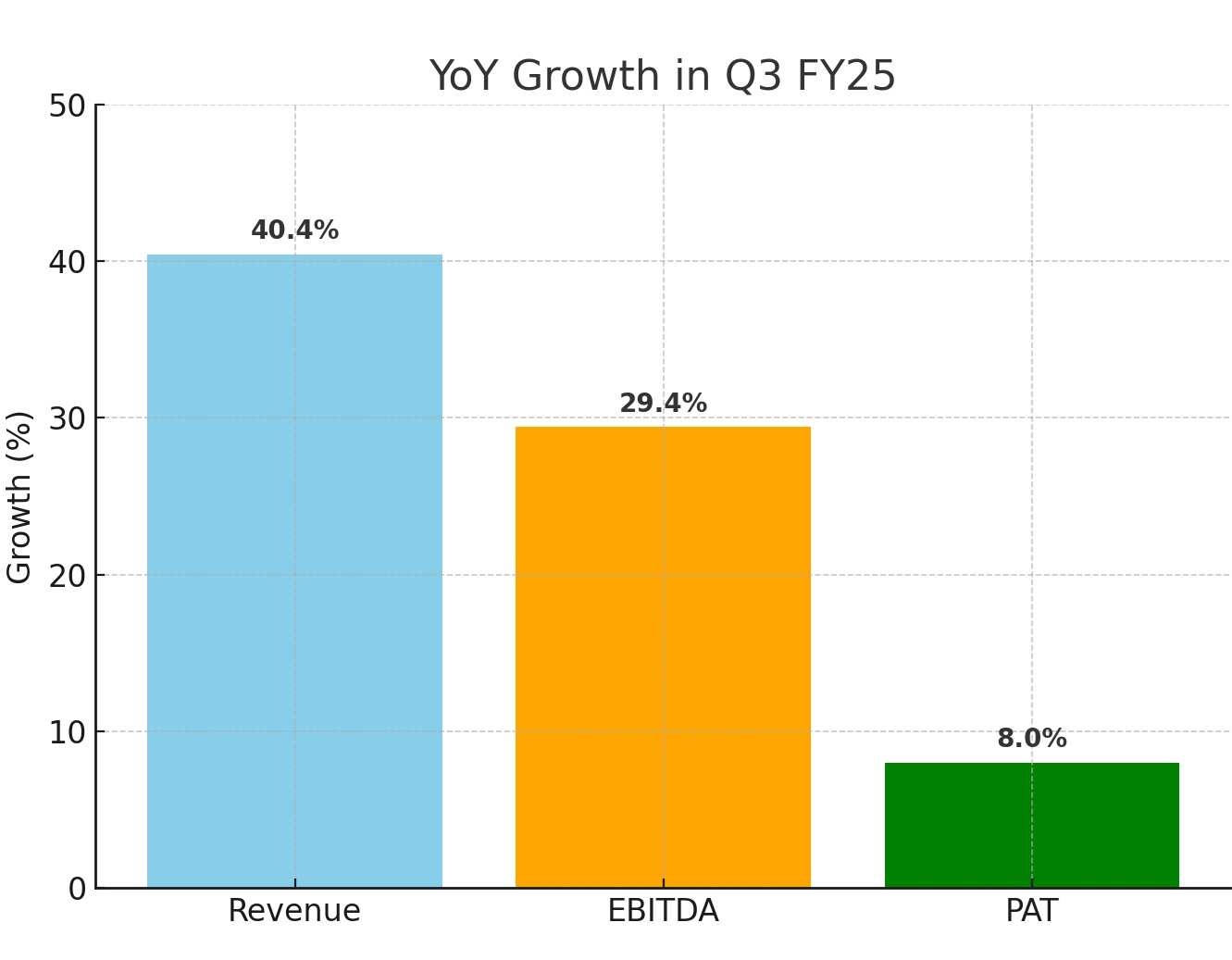

Previous quarter’s performance

In the third quarter of FY25, the company saw growth in its net profit, revenue, and EBITDA as follows:

- Revenue: Up by 40.4 per cent

- EBITDA: Rose by 29.4 per cent

- Net profit: Increased 8 per cent compared to the same period last year.

Moreover, for the first nine months of FY25, its average revenue earned per operational bed (ARPOB) was around Rs 76,000 which is higher than major hospital firms peers like Medanta, Apollo Hospitals, and Fortis Healthcare.

Moreover, for the first nine months of FY25, its average revenue earned per operational bed (ARPOB) was around Rs 76,000 which is higher than major hospital firms peers like Medanta, Apollo Hospitals, and Fortis Healthcare.

Anurag Dhole is a seasoned journalist and content writer with a passion for delivering timely, accurate, and engaging stories. With over 8 years of experience in digital media, she covers a wide range of topics—from breaking news and politics to business insights and cultural trends. Jane's writing style blends clarity with depth, aiming to inform and inspire readers in a fast-paced media landscape. When she’s not chasing stories, she’s likely reading investigative features or exploring local cafés for her next writing spot.

- ANURAG DHOLEhttps://indiatadkha.com/author/bitlancetechhubgmail-com/

- ANURAG DHOLEhttps://indiatadkha.com/author/bitlancetechhubgmail-com/

- ANURAG DHOLEhttps://indiatadkha.com/author/bitlancetechhubgmail-com/

- ANURAG DHOLEhttps://indiatadkha.com/author/bitlancetechhubgmail-com/